Safe, but not always: A liquid funds primer

By: Tavaga Research

Liquid Funds Meaning

Liquid funds are money-market instruments that invest in securities, with maturity terms ranging from one to 91 days, such as treasury bills (T-bills), certificate of deposits (CD), commercial papers (CP). These are fixed-income instruments.

In a liquid fund, the fund manager’s main objective is capital preservation to ensure the portfolio is liquid. Liquid funds focus on the safety of the investment instead of high returns. Therefore, the returns on liquid funds are perceived to be low-risk because the underlying investments are mainly debt-market instruments.

What are the costs of liquid funds?

While we may go about investing in any of the liquid funds offered by fund houses, there will be a small fee which the fund house charges for professionally managing our money, and it is called the expense ratio.

The expense ratio represents the annual maintenance charge of a scheme. It is expressed as a percentage of the fund’s assets under management (AUM). The fund’s operating expenses include spends on administration, management, and advertising.

SEBI (Securities and Exchanges Board of India) stipulated the expense ratio should not exceed 2.25 percent of the AUM. Typically, liquid funds hold the securities until their maturity and charge minimal expense ratio.

Liquid Fund Returns, Risk, and Benefits

Liquid Fund Returns

The returns on liquid funds are perceived to be low-risk because the underlying investments are mainly debt-market instruments.

Tavaga is everything you need to start saving for your goals, stay on track, and achieve them in time.

Download Now:

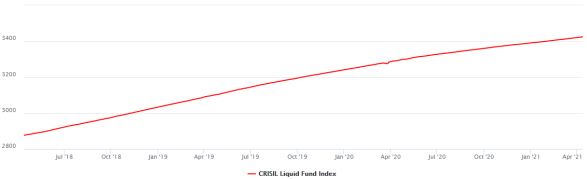

Historical data shows the returns on liquid funds to have been between 6 and 7 percent. We take a look at Crisil’s liquid fund index, which gives a bird’s eye view of liquid funds’ aggregate performance.

Benefits of liquid funds

They may be attractive to a retail investor for a host of reasons such as:-

- No lock-in period

- Withdrawals are processed within 24 hours

- Low exit load

- High liquidity

Liquid Fund Risks: Is it safe to invest in liquid funds?

The safety of a financial instrument is often synonymous with its volatility. The less volatile it is, the safer it is considered because of the chances of preserving our capital are higher.

Liquid funds are also subject to constraints imposed by SEBI, for example, liquid funds have to maintain at least 20 percent of the AUM in liquid assets such as cash and Government securities. Liquid funds also have sector exposure limits that make these mutual funds extremely well-diversified across the debt universe.

However, to earn money, there will always be some risk figured in. We list out three of the main risks with liquid funds below:

Interest rate risk

Changes in the repo rate and bank-lending rates have an effect on debt-market instruments. The prices of debt-market instruments and the interest rates are inversely related. When the economy does well, the interest rates are often raised. But rising interest rates lead to a fall in debt-instrument prices.

This is why equity markets’ performance is often at odds with debt-market instruments’ prices because the former looks up when the economy is on a roll, while debt-market instruments plummet.

The degree to which the prices of debt-market instruments are affected by interest rates is also dictated by their maturity periods. If the maturity period is short then the sensitivity of prices to changes in interest rates is low as well.

This is a mitigating factor for liquid funds. Liquid funds have short tenures, ie. they mature in a short period of time. Hence, the risk of an adverse impact of an interest rate hike is relatively small for liquid funds, compared to other instruments.

Credit risk

Credit risk is the risk of the issuer (ie. the company which issues the debt securities) defaulting on their debt payments.

We got a glimpse of such a scare last year when debt funds were caught in the fallout of a rating downgrade of a non-banking financial company (NBFC), IL&FS.

In September 2018, it was downgraded from an AA+ rating to a D, owing to a series of defaults in its CPs or bonds. Other non-banking lenders such as DHFL and Reliance Capital came under the scanner for defaults, leading to the entire NBFC sector finding its access to credit sources curtailed.

Debt funds, which reportedly used to park nearly 20 percent of their assets in NBFCs’ short-term CPs, saw their net asset values (Navs) nosedive as more NBFCs came under the suspicion of being possible defaulters. Some of the fund houses offering debt funds, saw their Navs decreasing by over 1 percent on a single day, considered a huge fall.

The pall of gloom in the banking sector currently, owing to bad-loan books, is yet to affect debt-market instruments, though.

Concentration risk

If a fund has a high amount of holdings in a particular security or a particular group of securities (say, a sector-specific fund), then any fluctuations owing to company-specific or sector-specific causes will pose a risk. This is called concentration risk.

However, liquid funds run a low concentration risk because it is not restricted to a particular section of securities.

Liquid funds vs FDs

Are Liquid Funds better than FDs?

Fixed deposits (FDs) figure as one the best ways to invest, traditionally. Investors looking to eschew high-risk avenues for investments, even at the cost of greater rewards, have been known to opt for FDs. Liquid funds, too, have been preferred by a similar set of investors with low-risk appetite.

An FD provides a higher interest rate than bank savings deposits. Its basic structure has us invest a lump sum with the FD-issuing house (banks or NBFCs), and earn interest on our deposit. Generally, FDs offer an interest rate of around 5-7 percent, which varies depending upon the FD offering, as well as the state of the economy. Liquid funds, as mentioned often give returns a notch higher.

An FD’s safety or assurance of capital preservation is dependent on the issuing bank’s credit-worthiness. The recent PMC Bank fallout, locking thousands of investors out of their FD accounts, has shown us the pitfalls of taking a bank’s dependability for granted. Of course, liquid funds, too, have to be assessed for their credit risk exposure after the IL&FS crisis.

An FD is taxed in the tax slab of the individual. So, if we are in the highest tax bracket, then our FD interest earnings will be hard hit by taxation.

Here is a lowdown on the differences between a liquid fund and an FD:-

Source: Tavaga Research

Liquid funds vs ETFs: Why are ETFs better than Liquid Mutual Funds?

Exchange-traded-funds or ETFs are investment funds that trade on a stock exchange. The underlying securities passively mirror the composition of the index of a particular exchange (stock, debt, or commodities).

In the case of ETFs, the composition of the underlying securities is known to us before we invest, while for liquid funds, the constituents are not known.

Even though liquid funds are called that, they might in effect, be less liquid than ETFs.

We can trade (buy or sell) an ETF throughout the trading day on the exchange it is listed on. The price is the price at that moment, similar in nature to a regular stock unit.

But liquid funds, much like other mutual funds, are dictated by their day-end Navs. When purchasing or selling a liquid fund unit, we end up paying the Nav of the previous day, if we invest before 1:30 pm on a trading day, as that is the cut-off time for liquid fund trading orders. Hence, with ETFs, we get more real-time prices (influenced by market forces) than with liquid funds.

We would still need to keep in mind the ETF in question, though. We should select ETFs with higher trading volumes, as the availability of some other ETFs is low, and hence, spontaneous trading on those might be a challenge.

Are liquid funds tax-free?

Liquid funds, just like other mutual funds come in two forms — growth and dividend.

In growth plans, the dividends of the fund are reinvested, hence the value of the units keeps on increasing due to capital appreciation as well as dividend reinvestment.

If the units are redeemed before 36 months (or three years), then short-term capital gains tax is applied according to the tax slab of the investor. If we hold the units for more than 36 months, then long term capital gains tax gets applied at a rate of 20 percent, albeit with the benefit of indexation.

As per the recent changes introduced by the Finance Act 2020, for all dividends received on or after April 1, 2020, dividends are taxable in the hands of the investor. For all dividend plans, the dividend received by the investor is added to the investor’s income and taxed according to the applicable tax slab.

In addition to the taxable dividend, if the dividend amount received is greater than Rs 5,000 in a financial year, the fund houses are required to impose 10 percent TDS. For example, if the dividend due is Rs 8,000 for Mr. A, the fund will charge TDS @10% on Rs 3,000, which amounts to Rs 800. Therefore, Mr. A will receive a dividend of Rs 7,200, which will be taxable as per the slab rate applicable to Mr. A.

However, due to COVID-19, the TDS rate of 10 percent has been reduced to 7.5 percent. The reduced rate is applicable for dividend distribution from 14 May 2020 until 31 March 2021.

Best liquid funds in 2021

The performance of liquid funds is dictated by the factors we have enumerated. It is best to check their status at the time of investment than go by historical performance.

Top-performing liquid funds in India (Data as on April 13, 2021):

How to pick a liquid fund?

When investing in a liquid fund, we should ideally aim for a comparatively low expense ratio (ie. management fees etc, charged from us, irrespective of the fund’s performance, should be less) and concentration risk (ie. should have more diversified underlying securities). It should be holding securities with a comparatively high credit rating and the fund house should have a credible track record (ie. consistent returns on its schemes).

We may refer to ratings by credit-rating agencies such as Icra, Care, Crisil. While not always foolproof, they rate funds based on their underlying securities and consider the findings as their proprietary research.

Another thumb rule to guide the average investor is a high AUM. Institutional investors park sizeable capital in liquid funds. Should the AUM of the fund be less, the day a large redemption request is forwarded by one of them, the Nav can fall drastically, denting the worth of our portfolios.

How to invest in liquid funds?

Armed with our Pan card, Aadhar card, and identity documents for KYC (Know your customer) processing, we may proceed to buy liquid fund units.

KYC can be done either online or offline. The offline route will take us to the fund house’s nearest office or a broker’s. For online KYC, we may resort to Aadhar-based electronic KYC.

When ready to buy units, we may put in the request with the fund house issuing the liquid fund or with brokers/aggregators.

Liquid funds come in two versions of direct and regular plans. The latter is suited for those looking to take advice from middlemen such as brokers on which plan to choose. Those investors choosing direct plans, do so for their low total expense ratio comprising administrative fees, brokerage charges, and distributional expenses since direct plans don’t charge for brokerage.

Liquid funds, then, are one kind of investment vehicle and may be used for certain financial goals. For example, ETFs being a veritable part of passive investing, are best suited to create wealth over a long period of time. Whereas, liquid funds can help with investing our money for a short period of time, mostly for short-term money goals or for parking our investments as we near our deadlines.

Liquid Fund Redemption: How does redemption work for liquid funds?

The first step is to place the redemption request. The time of redemption request with the fund house is a deciding factor for the NAV price, which applies to the units being redeemed. If the request is placed before the cutoff time, the lower of the same day’s NAV or previous day’s NAV is applicable. If the request is placed after the cutoff time, the lower of the same day’s NAV or next day’s NAV is applicable.

Typically, the redemption is completed one to two days after the redemption request is placed with the fund house. However, after a recent SEBI guideline for liquid funds, investors may withdraw up to Rs 50,000 or 90 percent of the investment, whichever is lower, per day per scheme. The redemption requests falling under the category of the recent regulation are processed instantly, with the money transferred to the investor’s bank account within minutes using the IMPS facility.

Best Liquid Funds with Instant Redemption

Sundaram Mutual Fund recently launched the instant redemption facility wherein the investors can opt for instant redemption up to Rs 50,000 or 90% of the investment amount. Along with Sundaram Mutual Fund, the following liquid funds offer instant redemption:

- Kotak Liquid Fund

- ICICI Prudential Liquid Fund

- DSP Liquidity Direct

- Nippon India Liquid Fund

- Aditya Birla Sun Life Liquid Fund

Liquid Funds Exit Load

Exit load charges follow the given schedule for the respective days after subscription:

Day 1 – 0.0070%

Day 2 – 0.0065%

Day 3 – 0.0060%

Day 4 – 0.0055%

Day 5 – 0.0050%

Day 6 – 0.0045%

Day 7 Onwards – 0.0000%

Liquid funds have no exit load after six days of investment.

Nine key MF terms explained:

AMC

AMC or an asset management company is a company that professionally manages the money, either pooled or of a family or an individual, in different asset classes. It makes the investment process more systematic.

Its clients could include high-net-worth individuals, hedge funds, pension funds, and retail investors (for products like MFs, index funds, ETFs). In the case of MFs and ETFs, we also call the AMC as the fund house.

AUM

When an AMC manages a pooled sum of money from clients, the invested amount is called the assets under management or AUM.

NAV

The net asset value or NAV represents the current unit value of the fund. It is similar to a share’s current market price (CMP).

We calculate the NAV by adding the market value of all the assets in the fund, minus all liabilities, and dividing the amount by the number of units issued by the fund house.

Entry load

It used to be the fee levied by the AMC when an investor joined the scheme, to cover its distributional expenses (for distributing the fund or scheme among customers, brokers).

However, in August 2009, Sebi mandated that MF companies will not charge entry load.

Exit load

It is the fee levied by the fund house to discourage investors from early withdrawals. Typically, in most MFs, AMCs levy an exit load of 1 percent of the Nav, if the units get sold within a year of purchase. There is no exit load if we sell units off after a year of holding them.

Of course, exit loads vary across fund houses and products. ln debt-related MFs, including liquid funds, the period in which exit load is valid can be just one day of purchase because the maturity period itself is short.

NFO

A new fund offer or NFO is the offer of a new fund, by an AMC. The funds raised through an NFO, are invested by the fund house in the markets and thereupon the units are issued to the investors.

Such an offer behaves similarly to an initial public offering (IPO) of equity shares of a company. Just as new shares of a just-listed company are distributed among investors in an IPO, new units of a new fund are distributed in an NFO.

SIP

A systematic investment plan or SIP is a way of investing in the market.

We choose a sum of money to invest at regular intervals with a Sip and it helps us be systematic in our investments. It keeps us from bothering with timing the market with lump sums.

SIPs can be done in ETFs as well as MFs.

STP

A systematic transfer plan or STP is a way of transferring our lump sum investment to a Sip.

A lump sum is invested in a debt instrument and an STP mandate transfers a certain amount from it to an equity instrument through the Sip route. Of course, this is the general concept and we may tweak the arrangement according to our needs and offerings by the AMC.

STPs help in a way similar to a Sip, by letting us invest in markets continuously, irrespective of market swings.

SWP

A systematic withdrawal plan or SWP is a way of withdrawing a specific amount of money at regular intervals. Generally, this is suited for retirees who need a continuous flow of income and want to avoid timing the market on when to redeem or withdraw their earnings. A way to regularly withdraw works like a pension for retirees.